Choosing the right car loan term in the UAE is essential for managing your finances effectively. The loan duration impacts your monthly payments, interest costs, and the overall affordability of your car purchase. Should you opt for a shorter term with higher payments or a longer one with lower installments? This guide breaks down the pros and cons of each option, helping you make the best financial decision.

In this guide, we’ll explore the pros and cons of different car loan terms, factors to consider, and expert tips to help UAE buyers make the best choice for their needs.

What Are Car Loan Terms in the UAE?

In the UAE, car loan terms typically range between 12 months (1 year) and 60 months (5 years). The duration of the loan determines:

- Monthly payments: Shorter terms have higher payments, while longer terms offer smaller installments.

- Interest costs: Shorter terms result in lower total interest, while longer terms increase the overall cost of borrowing.

Banks and financial institutions in the UAE offer both flat-rate loans and reducing-balance loans, with interest rates varying based on the loan term, the borrower’s credit score, and other factors.

Factors to Consider When Choosing a Car Loan Term in the UAE

Selecting the ideal loan term depends on your financial situation and preferences. Here are the key factors to consider:

1. Monthly Budget

Your ability to manage monthly payments is a crucial factor:

- Shorter term: Higher monthly payments but less interest paid overall.

- Longer term: Lower monthly payments but higher interest over time.

2. Total Interest Paid

While longer terms make monthly payments affordable, they increase the total interest you’ll pay. For example:

- AED 80,000 loan at 3.5% interest for 3 years = AED 4,200 total interest.

- AED 80,000 loan at 3.5% interest for 5 years = AED 7,000 total interest.

3. Vehicle Depreciation

Cars in the UAE depreciate rapidly—by 20-30% in the first year and about 50% over 5 years. If your loan term is too long, you may owe more on the loan than the car’s resale value, a situation known as negative equity.

4. Early Settlement Fees

If you plan to repay the loan early, remember that UAE banks often charge an early settlement fee, typically 1% of the outstanding balance. A shorter term minimizes this risk.

5. Long-Term Financial Goals

Consider your other financial goals. A longer loan term might free up monthly cash flow for savings or investments, but it increases your overall debt burden.

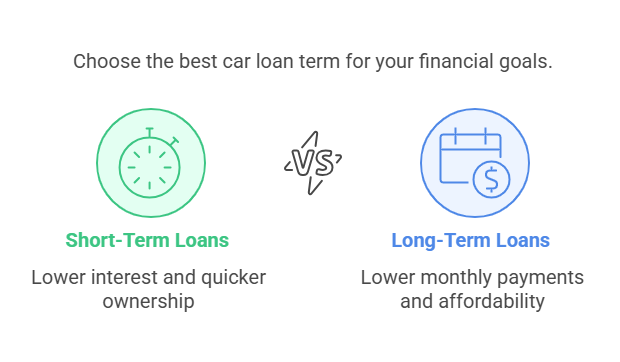

Short-Term vs. Long-Term Car Loans: Pros and Cons

Short-Term Car Loans (1-3 Years)

Pros:

- Lower Total Interest: A shorter term means less interest paid over the life of the loan.

- Quicker Ownership: You own the car outright sooner, giving you financial freedom.

- Better Resale Value: If you plan to sell the car, it’s less likely to depreciate below the loan amount.

Cons:

- Higher Monthly Payments: Larger installments may strain your budget.

- Limited Flexibility: Requires strong financial discipline to manage higher payments.

Long-Term Car Loans (4-5 Years)

Pros:

- Lower Monthly Payments: Easier to manage with a tight budget.

- More Affordable Vehicles: Allows you to buy a more expensive car with manageable payments.

Cons:

- Higher Total Interest: Increases the overall cost of borrowing.

- Risk of Negative Equity: You may owe more than the car’s value as it depreciates.

- Longer Financial Commitment: Limits your financial flexibility for other goals.

Ideal Car Loan Term in the UAE Based on Car Type

The type of car you’re purchasing can also influence the loan term you should choose:

1. New Cars

- Recommended Term: 3-4 years.

- Reason: New cars have a higher resale value for the first few years, minimizing the risk of negative equity. A medium-term loan strikes a balance between manageable payments and reasonable interest costs.

2. Used Cars

- Recommended Term: 1-3 years.

- Reason: Used cars depreciate faster than new ones, and shorter loan terms prevent you from owing more than the car’s value.

Example: Loan Term Comparison

Let’s compare how different loan terms affect monthly payments and total costs for a car loan:

- Loan amount: AED 80,000

- Interest rate: 3.5% (reducing balance)

| Loan Term | Monthly Payment (AED) | Total Interest Paid (AED) | Total Cost (AED) |

| 1 year | 6,780 | 1,320 | 81,320 |

| 3 years | 2,340 | 4,200 | 84,200 |

| 5 years | 1,460 | 7,000 | 87,000 |

Key Insights:

- A 1-year loan minimizes total costs but requires high monthly payments.

- A 5-year loan offers lower payments but increases total interest costs significantly.

Expert Tips for Choosing the Right Car Loan Term in the UAE

- Set a Realistic Budget: Before choosing a loan term, calculate your monthly expenses and determine how much you can comfortably allocate for car payments.

- Opt for a Down Payment: The UAE Central Bank requires a minimum 20% down payment. Paying more upfront reduces the loan amount, lowering monthly payments and total interest.

- Use a Car Loan Calculator: Utilize online tools to compare loan terms, monthly payments, and total costs. Many UAE banks offer loan calculators on their websites.

- Prioritize Shorter Terms for Used Cars: Avoid long-term loans for used cars, as they depreciate quickly and may lead to negative equity.

- Consider Refinancing Options: If you initially choose a longer term but your financial situation improves, you can refinance to a shorter term to save on interest.

- Factor in Insurance Costs: In the UAE, car insurance is mandatory and often tied to the car’s value. Ensure you account for these costs in your overall budget.

Conclusion: What’s the Ideal Car Loan Term in the UAE for You?

The perfect car loan term in the UAE depends on your financial goals, budget, and the type of car you’re purchasing. If you can afford higher monthly payments, a shorter term (1-3 years) saves you money on interest and reduces the risk of negative equity. However, if cash flow is a concern, a longer term (4-5 years) can make payments more manageable, albeit at a higher total cost.

Ultimately, the key is to strike a balance between affordability and minimizing overall costs. Take the time to compare offers, calculate potential savings, and ensure your car loan aligns with your broader financial goals.

For Car Loans in Abu Dhabi, Ras al Khaimah and Al Ain Car Financing is possible via Auto Loan vehicle Services Like MyCarLoan.ae